Introduction of the topic

Corona virus, commonly known as Covid-19, is an infectious disease that causes diseases in the respiratory system of humans. The term Covid 19 is an acronym derived from “New Corona Virus Disease 2019”. The coronavirus has affected our daily lives. The epidemic has affected millions of people, sickening or dying from the spread of the disease. COVID-19 is a new virus that is affecting the entire world badly as it spreads primarily through person-to-person contact. It spreads from person to person among close contacts within 6 feet. All governments, health organizations and other authorities continue to focus on identifying patients affected by COVID-19. Healthcare professionals these days face many difficulties in maintaining the quality of healthcare. As the world faces the coronavirus crisis, the pandemic has wreaked havoc and changed human lives forever. Its effects and adverse effects are felt long after the virus has subsided.

Last two years will become a case study of how the world forgot Economics, it was because of fear, it was because of disease, it was because of the war, but it was also because of impatience, and hoping that 2023 will not be part of this case study. Since the pandemic hit, the economy has been plagued by shortages, some caused or worsened by COVID and many not. Indeed, none of the supply crunches just cited coins, formula, antibiotics, veterinary services; early-childhood education has much to do with the virus still afflicting the world. Something deeper is going on. After the Great Recession, we went through a decade in which economic life was defined by a lack of demand. Now, after the COVID recession, we’ve entered a period in which economic life is defined by a lack of supply.

World Economic changes in 5 countries

World Bank President David Malpass has warned that the global economy faces a “dark situation” as the after-effects of the pandemic continue to weigh on economic growth, particularly in poorer countries. The organization’s forecasts indicated that the global economic growth of 5.5% in 2021 will decrease to 4.1% in 2022. Virus threats, reduced government aid, and reduced demand for goods are cited as reasons. But Chairman Malpass said he fears widening global inequality. “The biggest obstacle is the inequality in the system,” he said, adding that poor countries could be vulnerable to economic decline as they struggle to combat inflation. “The outlook for poor countries is still lagging behind. It causes economic insecurity in the country.” By 2023, economic activity in all advanced economies, such as the United States, the European region, and Japan, is likely to recover from the impact of the pandemic, the World Bank said. However output in developing and emerging countries is expected to decline by 4% from pre-Covid levels. Officials in many countries, including the United States, are now expected to raise interest rates to control price increases, and the World Bank president warned that high borrowing costs could hurt economic activity – especially in countries with weaker economies. Raising interest rates hurts people who borrow at floating rates, such as new businesses, women-owned businesses, and businesses in developing countries.

In addition, the World Economic Forum (WEF) warned that divergent economic growth in the recovery would make it difficult to cooperate on global challenges such as climate change. Widening disparities within and between countries not only make controlling Covid-19 and its variants more difficult, but also risk bringing the world to a standstill unless the world is able to take concerted action against these common threats that cannot be ignored,” WEF issued on 11 January 2022, notes in its annual Global Risk Report.

The World Bank’s Global Economic Prospects report shows that the world economy is set for the strongest post-recession expansion in 80 years in 2021 due to the pandemic. But the benefits are expected to be slow, as people have to bear the rapidly rising prices of virus strains, food, and energy. Globally, inflation has reached its highest rate since 2008, the report said.

The World Bank, which lends to countries around the world, further warned that constraints on supply chains and the easing of stimulus programs pose economic risks. Due to the spread of the Omicron and Delta Covid variants, the World Bank estimated the economic slowdown in the second half of 2021 higher than expected in its June forecast. It predicted a “pronounced slowdown” in 2022, with global growth forecast to fall further to 3.2% in 2023.

With the global economic slowdown, China’s growth rate is expected to drop to 5.1% from last year’s (2021) 8%. The World Bank forecasts a slowdown in the European region from 5.2% to 4.2% this year, compared to 5.6% in the United States in 2021.

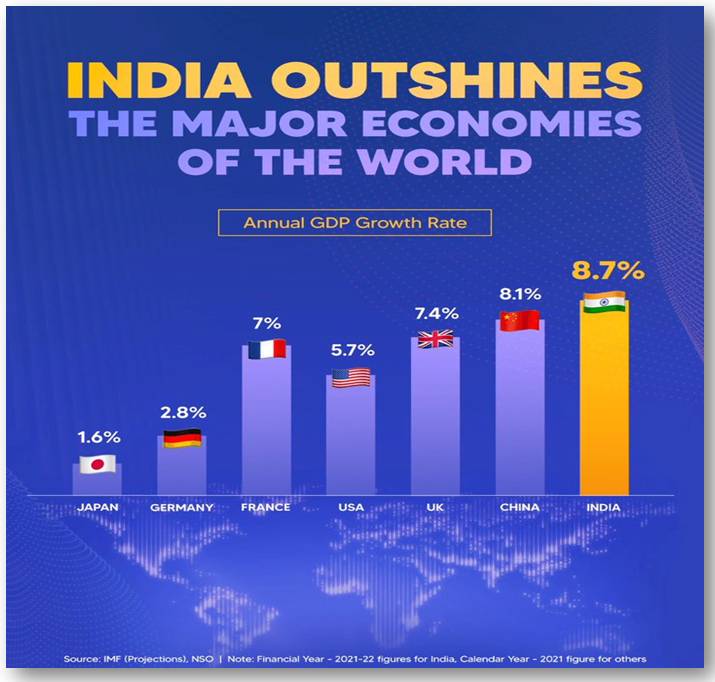

India’s growth rate this year is expected to rise from 8.3% to 8.7%, making it a unique opportunity. But many emerging markets will continue to suffer with additional challenges, such as low vaccination rates. For example, growth in Latin America and the Caribbean is expected to slow from 6.7% last year to 2.6% in 2022.The long tail of the pandemic and the fresh shock of a major ground war in Europe fundamentally changed the global economic narrative.

As a follow-up on the world economy that collapsed due to the Corona epidemic, the economic situation of those countries can be shown as a follow-up. Through the economic conditions of their countries, we can know that during economic recessions, some countries have improved more than the previous conditions. It is possible to learn how the economic situation of countries has developed and collapsed with some changes. To gain some insight into the economic changes that have taken place in the world after Corona pandemic America, China, India, France & South Africa can be presented as an example.

1.United States of America

This era, which began in 2018, was one of massive government spending. Congress approved $5 trillion in COVID-related stimulus, and the fed once again lowered borrowing costs to zero during the early pandemic, before raising rates to slow the rapid pace of cost increases. It is an era of good GDP growth, high inflation and rising GDP ratio.

The problem in the supply world is that shortages, along with rising costs, are keeping businesses and families from getting the things they want and need. USA has labor shortages due to COVID-related retirements, COVID-related disability and death, changes in immigration, and low-wage industries struggling to retain workers. The number of people coming to the US has fallen thanks to the Trump administration’s restrictive border policies and anti-immigration rhetoric: Immigrants added more than a million people to the population in 2016 and a quarter of that in 2021. At the same time, COVID pushed millions of older Americans into retirement, but some are now returning to the workforce; the virus killed thousands of workers and disabled millions more. Many industries have struggled to attract workers due to burnouts, dangerous working conditions, persistently low wages, or some combination of the three.

Covid-19 came as an emergency. It has become a catalyst for lasting economic change. The pandemic, now in its third year, has redrawn the map of the US economy, reshaped its workforce, and reshaped the toolkit available to its policymakers. All those shifts seem likely to outlast the health crisis that sparked them. American workers are on the move as the economy tilts away from its historic coastal strongholds. After the remote work revolution, they will be at home during office hours. Companies are scrambling to hire — but they’re also investing in machines, taking on automation and e-commerce. Entrepreneurship is on the rise. Politicians have discovered the power of direct payments that have boosted household and business finances during the pandemic and can return the next time there is a downturn. Consumers are grappling with the biggest jump in the cost of living in generations.

Source: IMF world Economic Outlook Update, January 2020

What all this means for the already sharp income and wealth divides is a key question for the post-pandemic era. The wealthiest have pulled further. The advantages of working from home tend to favor educated professionals. Low-income workers are winning raises in a tight labor market — but inflation is eating away at their gains. Then there’s the housing shortage, a long-running, GDP-sapping national scourge responsible for a variety of problems, including the homelessness crisis, declining fertility rates, low productivity growth and a lack of cool new music. For decades, places like New York and the Bay Area have created more new jobs than allowed for new housing, leading to higher prices and longer commutes. Those superstar cities have exported their deficits across the country in recent years.

2.People’s Republic of China

China’s economic growth has slowed sharply in the second quarter of 2022, official data shows. The massive toll has been fueled by widespread Covid lockdowns and cast doubt on whether it can meet its previously set growth target. Output contracted 2.6% between April and June from the previous quarter, the statistics bureau said, prompting many economists to revise their forecasts for the world’s second-largest economy.

The economy grew 0.4% in the second quarter on an annualized basis, the worst since the pandemic-hit first months of 2020, but even that was worse than the 1% consensus forecast by economists. The consultancy Capital Economics said the real figure was probably “even weaker than meets the eye” and suggested that the Chinese government – accustomed to trumpeting growth well above that achieved by western countries – could be trying to disguise the economy’s sluggishness. In January, China’s government predicted that the country’s economy – at the time, experiencing a strong recovery after an initial pandemic slowdown – would grow by 5.5% in 2022. But by the second quarter, unfortunately, Omicron was expanding rapidly. The strain of COVID-19 has forced the government to implement emergency containment measures in its most economically dynamic cities, including Beijing, Guangzhou, Shanghai and Shenzhen. The two-month Shanghai lockdown, in particular, dealt a devastating blow to growth, as the entire Yangtze River Delta was effectively sealed off from the global economy. It also dented business and investor confidence. Although they still have faith in the long-term prospects of the Chinese economy many entrepreneurs and investors (both foreign and Chinese) are more cautious than ever about doing business there, at least in the short term. The effects of the shift are sure to linger even after economic activity – which has not recovered for more than three months since the lockdown was lifted.

According to official data released by China’s National Bureau of Statistics, the country’s industrial output growth, which measures activity in the manufacturing, mining and utilities sectors, fell to negative 2.9% in April 2022 from 5% in March 2022.The COVID-19 restrictions had a major impact on consumer spending in China as retail sales in April 2022 fell 11.1% year-on-year. With millions of people confined to their homes due to the lockdown, consumption dropped significantly. China’s job market also suffered, with the unemployment rate rising to 6.1% in April 2022 from 5.8% in March 2022, the highest level since February 2020. The unemployment rate among young adults aged 16-24 reached an alarming 18.2% in April. 2022.

China’s stock market index, the Shanghai Composite, widely regarded as the benchmark for China’s stock market performance, fell 17.5% in early May 2022 from the start of January 2022.

Source: IMF world Economic Outlook database

The manufacturing sector suffered the most as the cumulative growth rate slowed from 7.3% in February 2022 to 3.2% in April 2022. Crippled production and disruption of supply chains caused by the zero-COVID policy in many cities in China led to the sharp decline.

3.Republic of India

India’s growing role in the global economy, supported by a thriving service industry and a strong industrial base, is increasingly difficult to ignore. But as Commerzbank’s chief representative in Mumbai, Peter Bourne, explains, obstacles stand in the way of subcontinental prosperity. India’s economic growth trajectory in recent years has been nothing short of impressive. With a nominal GDP of US$2.8 trillion, the South Asian nation is now the sixth largest economy in the world and the third largest by purchasing power parity.

The human and economic costs of the Covid-19 pandemic were severe, especially after the outbreak of the delta strain in the spring of 2021. But India now appears to be turning a corner, with 1.6 billion doses of vaccine administered across the vast and diverse country. Many economic indicators, chief among them stock markets that reached record highs, suggest a strong recovery is on the cards. The country’s foreign exchange reserves of US$630 billion, the fourth largest in the world, protect it from further external shocks. It is this culture that has attracted established companies from many developed countries to outsource their services to India. India’s IT sector alone generated $191 billion in revenue, employing over four million people across the country.

It is not just the services sector that is finding a market beyond India’s borders. The country now ranks globally as the second largest supplier of food and agricultural products, coal, cement and steel, and also holds the position of third largest supplier of electricity in the world.

The pandemic has only served to underscore the important role India now plays in global markets. Having already achieved the status of the world’s largest producer of generic drugs, India is now also the leading producer of Oxford-AstraZeneca and Covaxin Covid-19 vaccines, meeting more than 50 percent of the global demand for vaccines.

The economy shrank by 6.6% in fiscal 2021 due to the pandemic and showed a mild recovery in fiscal 2022 when it grew by 8.7%. However, the impact varied across states, with some states experiencing less of the virus, while others were more able to withstand the shock. At one end of the spectrum, Bihar recorded the fastest positive growth (2.5%); Kerala was at the other end, which shrank by 9.2%.

Several main factors and changes in the economic sector seen in India after the outbreak of the Covid epidemic can be identified.

Not all states will see their gross domestic product (GDP) shrink in FY 2021, leading to a different permanent loss of GDP across states by FY 2022.

In terms of growth (before COVID-19 and with the pandemic-induced hit), the better placed states are Bihar, Tamil Nadu, West Bengal and Andhra Pradesh. Kerala, Maharashtra, Uttar Pradesh, Punjab, Rajasthan, Odisha, Jharkhand and Madhya Pradesh fare relatively worse.

Agriculture moderated the impact of the pandemic on growth among states. This suggests that states with a higher share of their GDP in agriculture on average may have contracted less in FY21.

Conversely, states with a relatively heavy reliance on connectivity-intensive services were hit harder during the pandemic.

Interestingly, low-income states do not appear to have been hit as hard by the pandemic’s hit to growth among states.

The sharp increase in inflation in the current financial year has been reflected in many states. Thirteen states at large have recorded higher inflation than the national average so far this fiscal, with Telangana, Maharashtra and West Bengal recording the highest inflation. Most states experiencing peak inflation are wealthy states

Financial stress, as measured by debt default levels, has increased across states over the past two years. Bihar, Kerala, Punjab and Rajasthan are particularly financially vulnerable, and their debt (as a percentage of GDP) is projected to be the highest among states this fiscal as well. Andhra Pradesh, Bihar, Kerala, Madhya Pradesh, Punjab, Rajasthan and West Bengal saw their finances worsen, with debt/debt exceeding 35%.

The evolution of India’s policy landscape is also matched by a changing outlook on the country’s trade relations. Recent tensions with neighboring China have prompted India to focus on strengthening ties elsewhere.

Source: IMF (Projection) NSO | Financial year 2021-22

4.French Republic

France is one of the leading European economies after Germany and France. The country has considerable value in the export of goods and services. The country has shown a significant increase in manufacturing operations including food and beverages, machinery and equipment and chemicals. Monetary policy, structural reforms and economic conditions have encouraged exports and investment in the country. However, the effects of global uncertainties and social conflicts have assessed on activities in 2018. Consumption and growth will benefit from increased purchasing power of households. France’s GDP growth is expected to remain close to 1.3% in 2019-20, according to the OECD. Moreover, France has more than 18,000 companies and more than 380,000 employees in the manufacturing sector. The country’s agri-food industry is the main contributor to the country’s economy, earning $170 billion in revenue in 2017.

France is facing a major challenge in the recession due to the impact of the COVID-19 pandemic. It has affected the country’s overall manufacturing capacity and has led to concerns about the slowdown in global demand and availability of raw materials. As a result, the country’s manufacturing and other industries have temporarily shut down their industrial operations. As of March 23, 2020, France has reported 15,821 cases of COVID-19 and 674 deaths due to COVID-19, according to the World Health Organization. Fears about business and jobs have risen sharply in France since February. In France, economic uncertainty appears to have suddenly grown more than concerns related to the level of risk posed by the coronavirus.

Based on industrial operations, France’s economy is classified into automotive, food and beverages, energy, electronics and electrical, aviation, BFSI, retail, travel and tourism, and others. The energy sector will be significantly impacted by COVID-19 due to the uncertainty of energy and energy generation and supply. According to French grid operator RTE, nuclear utilization is 3.6 GW below the average from 2015 to 2019, and a national decline in nuclear demand is expected due to the ongoing COVID-19 pandemic in the country. Furthermore, the spread of COVID-19 will delay the development of new wind farm projects further impacting the country’s energy sector further affecting wind farm deployment in the country.

During H1 2022, the French economy registered a significant shock, driven by inflation rates reaching the mid-80s. Inflation has accelerated significantly since March, and oil prices in euro have increased by 23% m/m, although this shock has dampened GDP growth, weighing on household consumption (-1.2% q/q in the first quarter). Far from deflating it completely, the French economy has benefited in parallel from the easing of Covid restrictions. This has led to a visible recovery in tourism and leisure activities, which were the main drivers of the positive growth performance during the 2nd quarter (+0.5% q/q).

However, without these positive contributions, growth is estimated to converge to 0%, with the following implications: Excluding tourism and leisure, the French economy grew by -0.2% q/q in Q1 and 0% in Q2: France 2022 H1 At the time, the economy was already on the brink of recession. And this situation was avoided by timely relaxation of covid restrictions.

France is the seventh largest economy in the world and the second largest in the Euro Area. The biggest sector of the economy is household consumption (55 percent) followed by government expenditure (24 percent) and gross fixed capital formation (22 percent). Exports of goods and services account for 29 percent of GDP while imports account for 31 percent, subtracting 2 percent from total GDP.

Some understanding of how the economic situation of France as well as the economic powers of the European region and other European countries has changed according to each quarter in the years 2021 and 22 can be obtained by using the table below.

Source: Eurostat National Statistics Institute

The French economy recovered quickly after the coronavirus crisis, thanks in particular to the acceleration of the vaccination campaign and strong public assistance measures. Prompt and effective implementation of recovery and investment plans will support strong and sustainable growth. However, public expenditure has reached exceptionally high levels with a mixed performance that necessitates restructuring the fiscal framework to ensure the sustainability of public finances. Education and labor market integration policies should be better targeted with specific training efforts for youth and older workers. Strengthened support for the most vulnerable and least qualified should reduce inequalities, including territorial ones. The transition to a green economy is the other major challenge France must take on. Strengthening green investment is critical to accelerating the pace of emissions cuts, and implementing the necessary incentives to foster behavioral change, if needed, with targeted support for the most vulnerable.

Although France’s economy has shrunk to a certain extent after the corona virus, France can be pointed out as the main economic center of the European continent at present. The table above reflects that France is ahead when comparing the economies of each country in Europe.

5.Republic of South Africa

New research from the United Nations Development Program (UNDP) shows that COVID-19 will cause South Africa’s overall gross domestic product to fall by 7.9 percent in 2020 and slowly recover by 2024, a major setback in addressing poverty, unemployment and inequality.

South Africa’s economy contracted for the first time in 11 years in 2020 as the coronavirus lockdown disrupted the economy by disrupting trade and output.

According to a report released by Statistics South Africa, gross domestic product contracted by 7% compared to 0.2% expansion in 2019.It was the economy’s first annual contraction since 2009, when GDP fell by 1.5%.

The decline was “mainly due to decline (inactivity) in industry, commerce, restaurants and hotels,” StatSA said. But expansion in the fourth quarter of 2020 was stronger than economists expected, with GDP growing 1.5%. The growth between October and December was mainly driven by the industrial and commercial sector. The health crisis and restrictive measures have taken a heavy toll on Africa’s second-largest economy.

At the end of March, the government imposed one of the strictest lockdowns in the world, slowing the spread of the virus but also the economic outlook. The hospitality and tourism sectors have been particularly affected by measures such as night curfew and ban on sale of liquor.

It will take at least five years for South Africa’s GDP to return to 2019 levels. Poverty, unemployment and inequality are widening but steadily recovering. Female-headed households, people with low levels of education and the informal sector are the most affected. Those with access to technology and digitization are better off. Recovery will require innovative government policies and actions. COVID-19 is adversely affecting the achievement of the Sustainable Development Goals.

UNDP Senior Economist Fatu Li said: Lower poverty levels of South Africa will also increase by 46% in 2020, 66% under the optimistic scenario, 66% under the pessimistic scenario, 34% of middle-class households likely to fall into the vulnerable class, and about 44% more. People with permanent jobs who switch to the contract type are likely to fall back into poverty.

Particularly hard-hit populations are already poor female-headed households, people with only primary education, people without social assistance, black people and household heads who have been pushed from permanent employment to informal employment.

About 54% of these households that engage in informal employment are likely to fall into poverty. Income inequality is likely to increase due to perverse negative effects on an already disadvantaged population. It further observes that the economic sectors most disadvantaged by the outbreak of COVID-19 include textiles, educational services, food and accommodation (including tourism), beverages, tobacco, glass products and footwear. Small and medium-sized enterprises are most adversely affected.

South Africa remains a small, open economy and will be negatively affected by weakening global growth. The President must urgently address deficiencies in electricity, rail and port as well as water infrastructure, which are prerequisites for economic growth and stability as well as sustainable government revenue and debt levels. However, an impeachment, as happened under the RET leadership in the 2010s, risks destabilizing the country and plunging the economy into another lost decade.

The world’s poor and rich with growth

We can clearly see the economic imbalance of all the countries in the world after the corona pandemic. It is clear when we compare it with the economic indicators of different countries.

Resource – IMF #WEO

Considering the world economy after the corona epidemic, although economic recessions can be seen in certain countries, countries that maintain their economic pattern without falling can be presented with some examples. According to the reports of the year 2021, it can be pointed out as the first 10 countries among the countries with the richest economies in the world. Here’s a sneak peek at the top 10 as of October 2021

The Top 10 Richest Countries in the World (by GNI per Capita, Atlas Method, current US$ – World Bank)

- Liechtenstein – $116,440

- Switzerland – $84,310

- Norway – $78,180

- Luxembourg – $73,500

- United States – $64,530

- Ireland – $64,150

- Denmark – $63,070

- Iceland- $62,420

- Qatar – $56,210

- Singapore – $54,920

In the four-tier World Bank ranking system, the world’s poorest countries are classified as low-income economies. The ranking is based on each country’s gross national income (GNI) per capita, which is a measure of the country’s total income divided by its population. GNI is very similar to Gross Domestic Product (GDP) per capita. Both metrics measure the dollar value of all goods and services produced in a given country, but GNI also includes income earned through international sources (such as foreign investment or real estate). For that reason, GNI is considered a fairly accurate measure of a country’s economic health.

GNI is usually expressed in one of two ways. The first is in US dollars, calculated using a technique called the Atlas method for comparing each nation’s currency. The second is the “purchasing power parity (PPP) of the international dollar”, a hypothetical currency pegged to the value of the US dollar in a given year. Under the World Bank system, low-income countries are nations with a GNI (adjusted to current US dollars) of less than $1,046 as of July 1, 2021.

The 10 Poorest Countries in the World (based upon their 2020 GNI per capita in current US$)

- Burundi – $270

- Somalia – $310

- Mozambique – $460

- Madagascar – $480

- Sierra Leone – $490

- Afghanistan – $500

- Central African Republic – $510

- Liberia- $530

- Niger – $540

- Democratic Republic of the Congo (formerly Zaire) – $550

Source – The International Monetary Fund releases a definitive ranking of 236 countries and territories of the world.

Abbreviated

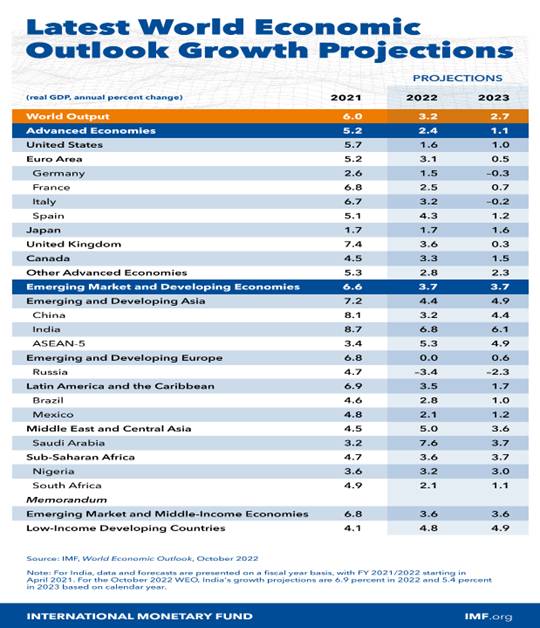

As central bank policy raises interest rates in the fight against inflation any global economic indicators for October and November point to slower growth or contraction. Forecasting agencies have been slashing growth projections, citing a number of challenges including policy tightening, inflation, Russia’s invasion of Ukraine and ongoing disruptions related to the COVID-19 pandemic. For example, in October, the International Monetary Fund (IMF) estimated that global GDP growth would slow to 3.2% in 2022 and 2.7% in 2023. For major economies in 2023, the IMF’s GDP growth estimates range from 4.4% for China. A contraction of -0.3% is for Germany. The US economy is expected to expand by 1% in 2023.

United States – The US economy expanded at an annualized rate of 2.6% in the third quarter of 2022, after contracting by −0.6% and −1.6% in the second and first quarters, respectively. Exports and consumer spending were the main sources of expansion.

Euro zone – Official data (Eurostat) shows that euro zone GDP expanded at a 2.1% year-on-year pace in the third quarter of 2022 (0.2% quarter-on-quarter). Among the largest constituent economies, Germany (up 0.3% quarter-on-quarter) and Italy (0.5%) led modest expansion. As of September, the European Central Bank’s full-year GDP growth projection for the euro zone is 3.1% in 2022, 0.9% in 2023, and 1.9% in 2024, with variations among member states.

China- According to the IMF following the impressive recovery from the initial impact of the pandemic, China’s growth has slowed and remains under pressure. GDP growth is projected at 3.2 percent for 2022, improving to 4.4 percent in 2023 and 2024.

India – Most forecasting agencies expect India’s economy to expand at a rate of 6.8-7% in FY 2022-23. In November, the OECD estimated that real GDP would slow to a pace of 5.9% in 2023-24, still the second-fastest in the G-20.

Overall, India is already the world’s fastest growing economy, recording an average gross domestic product growth of 5.5% over the past decade. Morgan Stanley has said that, India’s GDP could more than double from $3.5 trillion today to over $7.5 trillion by 2031. Its share of global exports could double during that time, giving the Bombay stock market 11% annual growth and reaching a market capitalization of $10 trillion. India has emerged as the fastest growing major economy in the world and is expected to be one of the top three economic powers in the world in the next 10-15 years due to its strong democracy and strong partnerships.

When considering the world economy after the corona virus, it is not easy to summarize the economic conditions of different countries separately. Therefore, by understanding the economic conditions of the powerful countries of the world and highlighting the economic conditions of each country according to different continents, possible to get a brief understanding of the world economy.

Source – IMF World Economic Outlook October 2022

If you look at the above note, you can clearly see how the world economy will change in the near future depending on the conditions of each country. In each of these countries, due to the covid crisis, the economy is undergoing major changes and the economic conditions are going up and down. Although some of the world’s most powerful countries have not had a severe impact on the economy due to Covid, it can be understood how the economies of the third world countries and low-income countries in different regions have shrunk to different levels due to Covid.Global economic activity is experiencing a broad-based and sharper-than-expected slowdown, with inflation higher than in decades. The cost-of-living crisis, tightening financial conditions in many regions, Russia’s invasion of Ukraine and the lingering COVID-19 pandemic all weigh heavily on the outlook. Global growth is forecast to slow from 6.0 percent in 2021 to 3.2 percent in 2022 and 2.7 percent in 2023. This is the weakest growth profile since 2001, excluding the peak of the global financial crisis and the COVID-19 pandemic. Global inflation is forecast to rise from 4.7 percent in 2021 to 8.8 percent in 2022, but is forecast to decline to 6.5 percent in 2023 and 4.1 percent by 2024. Monetary policy should be continuous and fiscal policy should be price-targeted to restore price stability. Cost of living is pressures while maintaining a sufficiently tight stance in line with fiscal policy. Structural reforms can further support the fight against inflation by improving productivity and easing supply constraints, and multilateral cooperation is needed to accelerate the green energy transition and avoid fragmentation. Thus, when considered completely, it can be clearly explained how the world economic conditions have been severely affected.

Hasitha Kasun Hapuarachchi

(Hasitha Kasun Hapuarachchi is Colombo based independent researcher mainly in the field of economics. He has completed his Bachelor of Economics special degree with first class honors at Gujarat University, Ahmedabad, India)

References –

- theatlantic.com/ideas/archive/2022/12/us-economy-supply-shortages

- worldbankgroup.org

- bbc.com/sinhala/world-59978338

- worldbank.org/en/news/podcast/2022/12/01/2022

- com/graphics/2022-us-economy-pandemic-recovery

- com/data-insights/equipment-amp-services-industrial-goods-amp-machinery-mining-transmission-and-distribution/chinas-economy-slows-down-amid-covid-19-lockdowns

- com/en/home/our-analysis/reports/2022/07/crisil-insights-indian-economy-states-of-aftermath

- commerzbank.com

- com/reports/5013562/impact-of-covid-19-on-the-french-economy

- https://www.oecd.org/economy/france-economic-snapshot/

- org/south-africa/press-releases/undp-releases-study-socio-economic-impact-covid-19-south-africa

- investec.com/en_za/focus/economy/sa

- https://worldpopulationreview.com/country-rankings/richest-countries-in-the-world

- https://worldpopulationreview.com/country-rankings/poorest-countries-in-the-world

- https://www.mckinsey.com/capabilities/strategy-and-corporate-finance/our-insights/global-economics-intelligence–executive-summary-november-2022

- https://www.morganstanley.com/ideas/investment-opportunities-in-india

- https://www.imf.org/en/Publications/WEO/Issues/2022/10/11/world-economic-outlook-october-2022

Nice article

“Thank you for sharing this; it is truly helpful.”